Gas Production Lags Way Behind Rig Growth Next Year

After updating rig count for higher gas prices, we have also refreshed our production model to account for more frac crews, completions, and downhole intensity.

XTO Sick Activity Trends

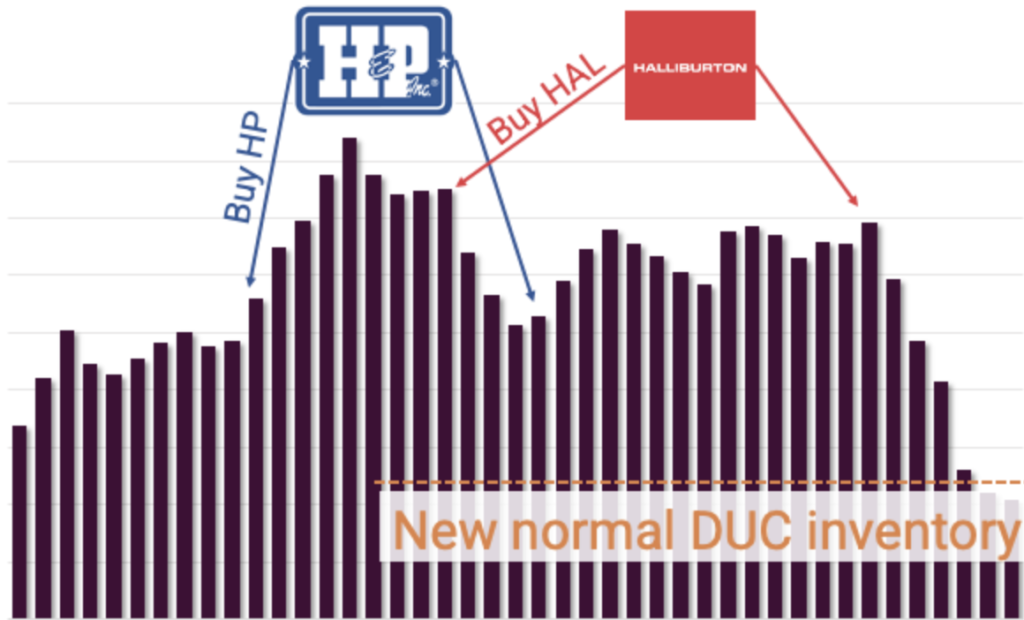

While privates are now building some DUCs, XTO (and many other publics) will also need to taper their DUC draws in coming quarters.

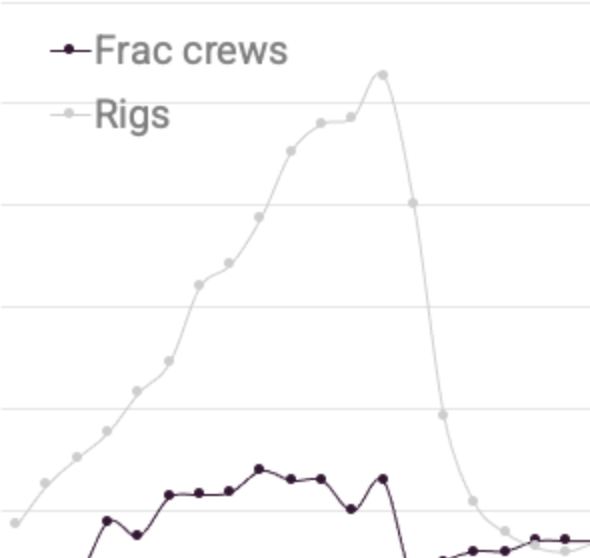

Operators Will Soon Need 30-60 More Fleets, FAST

For each of the last five years, E&Ps added 10-20% completion activity sequentially in Q1 – next year could be even better. The key drivers to next years surge will likely be…

Shale Data Trends – 2022E Surprises

In this report we think ahead to 2022, foreshadowing with predictive data some possible surprises that may materialize over the next 12-15 months.

September Slide Deck (2022E spend UP 30%+)

Our key takeaway is 2022E spending, which has the potential to be…

August Data Download (near-term very weak)

This week, we downloaded the bulk of our June / July data, with the biggest takeaway being relatively flat fully-utilized fleet counts since April.

DUC Update – Big Rebuild Coming

In this post, we have updated our DUC data as of Q3, identified what we believe is ‘normal inventory’ and presented our case for a big DUC rebuild over the next 12-18 months.

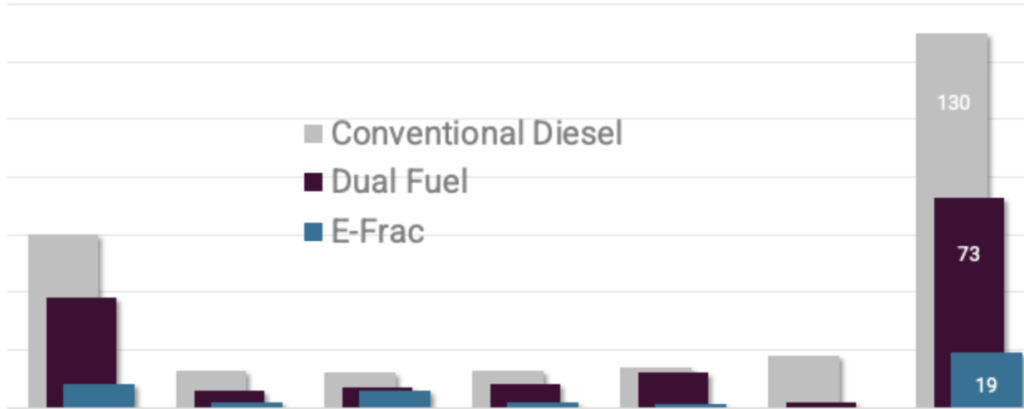

ESG Friendly Fleet Count – That Happened Fast

While the active fleet count has stagnated in recent months, the demand for ESG Friendly fleets has continued to surge.

Frac Supply Update – Approaching 17 Million HP

In recent weeks, we have updated our supply estimates, adding in multiple new entrants that are reviving old fleets.

Shale D&C Update ($60-70/bbl = 250 fleets / 550 hz rigs)

In this report, we have integrated recent monthly data (including the February winter freeze), with our longer term drilling & completions model. As part of this update, we have also taken a first look at 2022E in a $70/bbl scenario, which would likely push active frac crews over….