Lowering 2022E Frac Fleet Projections…

A year ago in this note, we talked about the potential for U.S. shale to maintain flat production at only 200 fleets.

First Set Of E&Ps Confirm Expectations (publics ain’t moving!)

While only a few E&Ps have reported so far, all have maintained 2021E budgets despite a 20% increase in the oil price since April…

PTEN Gaining Share

While activity from OFS companies so far (HAL, LBRT, BOOM, RES) has been lower than expected, we think PTEN will give a better look…

DUG Permian Conference Takeaways

Takeaways from the DUG Permian conference in Fort Worth this week.

Monthly Data Download – Flat Since April

In this post, we have updated our monthly completion data for members with Premium Memberships to download. This file contains most up-to-date fleet counts, completions, spuds, sand, efficiency, and intensity data. Key takeaways from the data refresh can be found written in this update.

Pricing Still Dismal

Although multiple E&Ps at the DUG conference this week acknowledged that OFS pricing was too low, the industry has still only been able to pass through meager price increases.

OFS Data Trends – Q2 Earnings

In these slides, we have highlighted the key data themes in OFS for the upcoming Q2 earnings season.

Public OFS Efficiency Gains – Putting Themselves Out Of Work

As private oilfield service companies put in the low bid, public OFS is pitching better and more efficient operations, which unfortunately is putting themselves out of work.

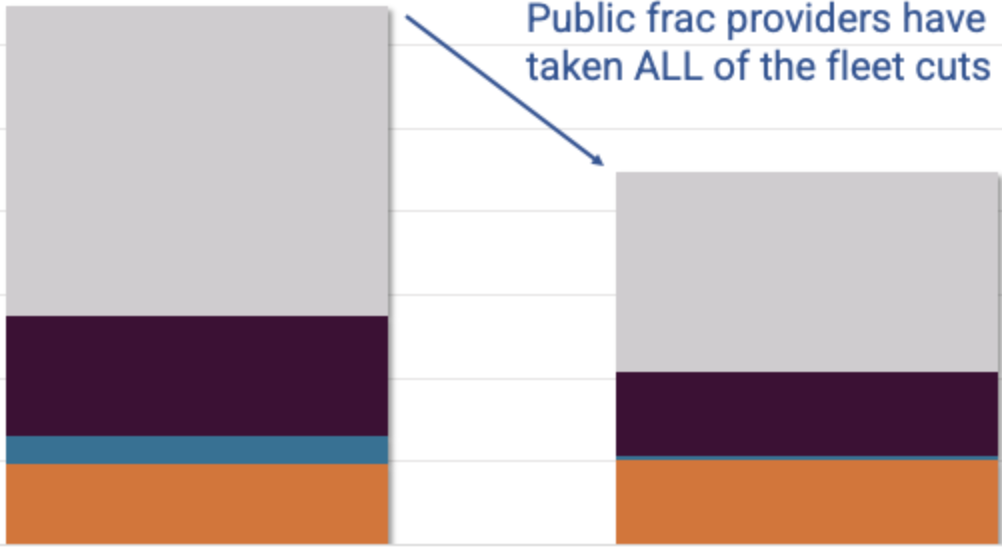

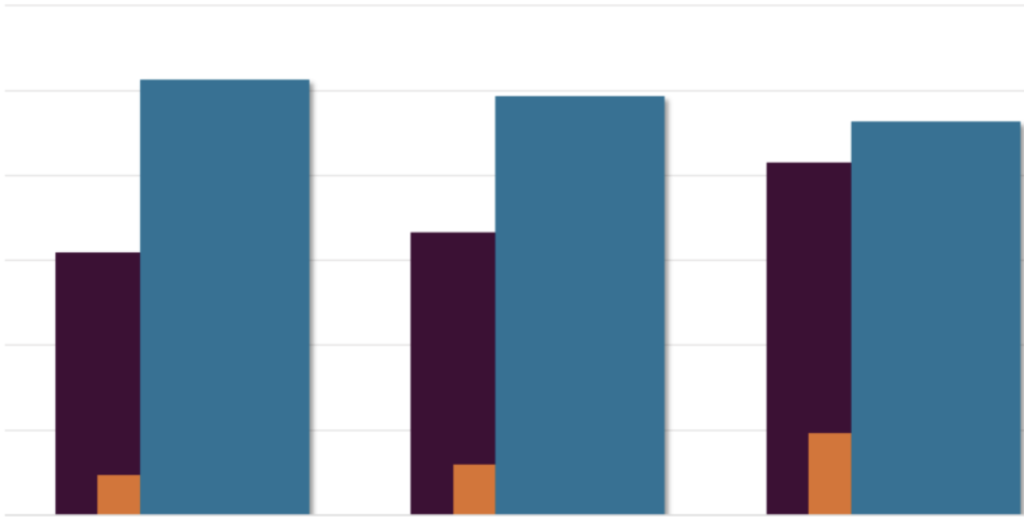

Private OFS Terribly Undisciplined

While public frac companies are showing discipline, privates are not…

Gas Production Not Keeping Up

Despite higher gas production in the latest EIA report this week, supply is not keeping up with strong demand…