July slide deck takeaways

Panel supply flows are great compared to 2022

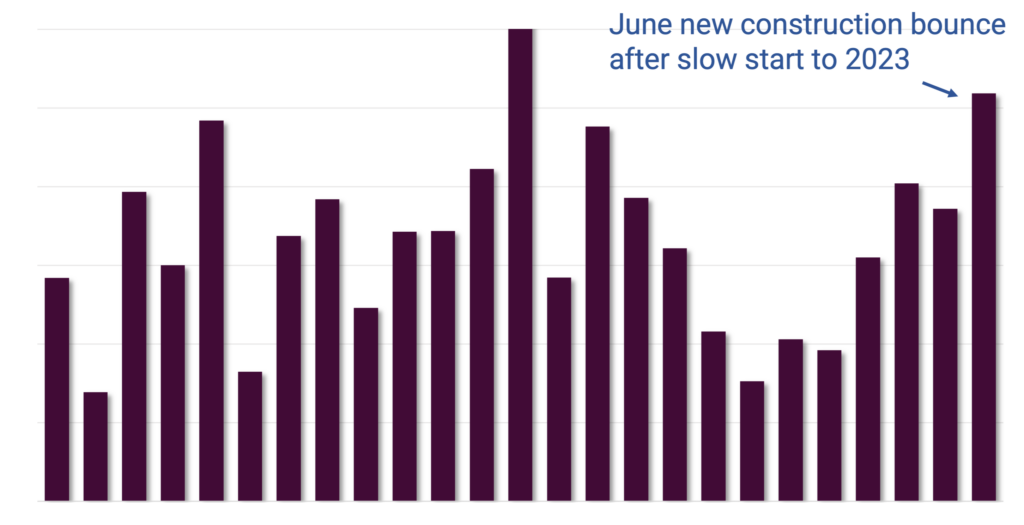

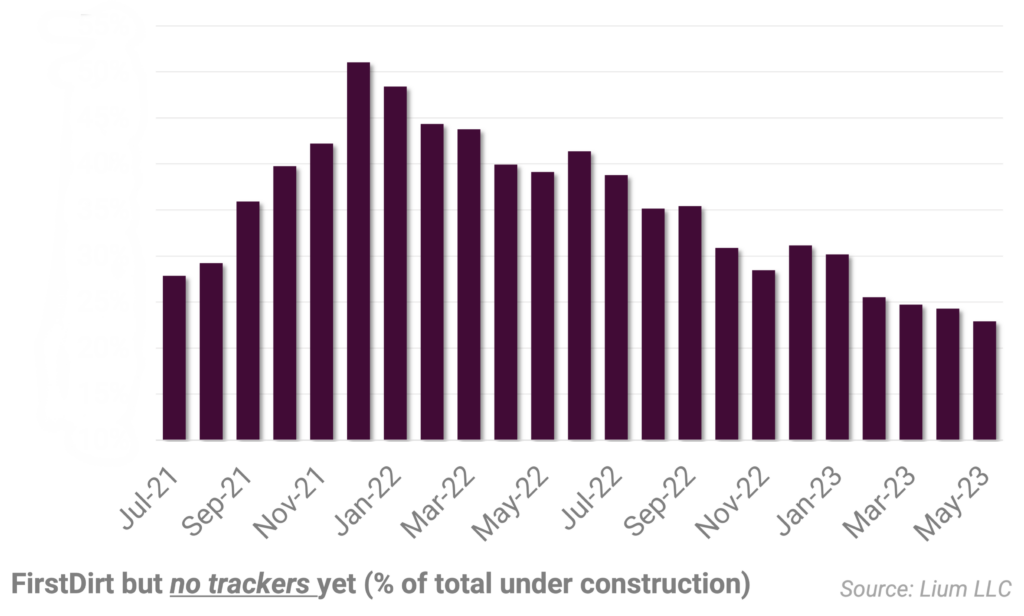

SOLARSAT™: June BIG month for new construction starts

roughly 2.5 GWac (30 GW annually) of new solar was started in June, suggesting that tracker demand can continue to grow despite mediocre new construction in early 2023

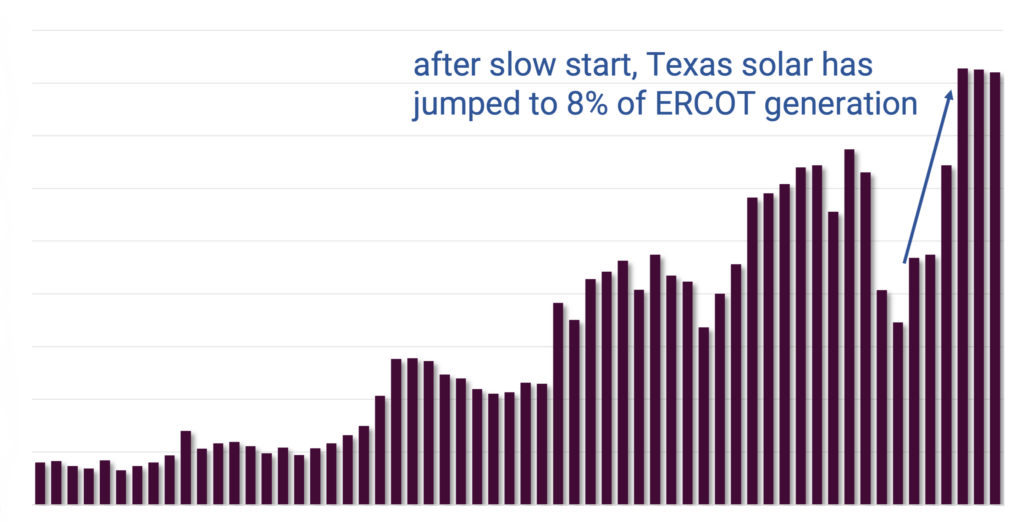

New generation, capacity, utilization data; NXT scores better than ARRY; FSLR on par

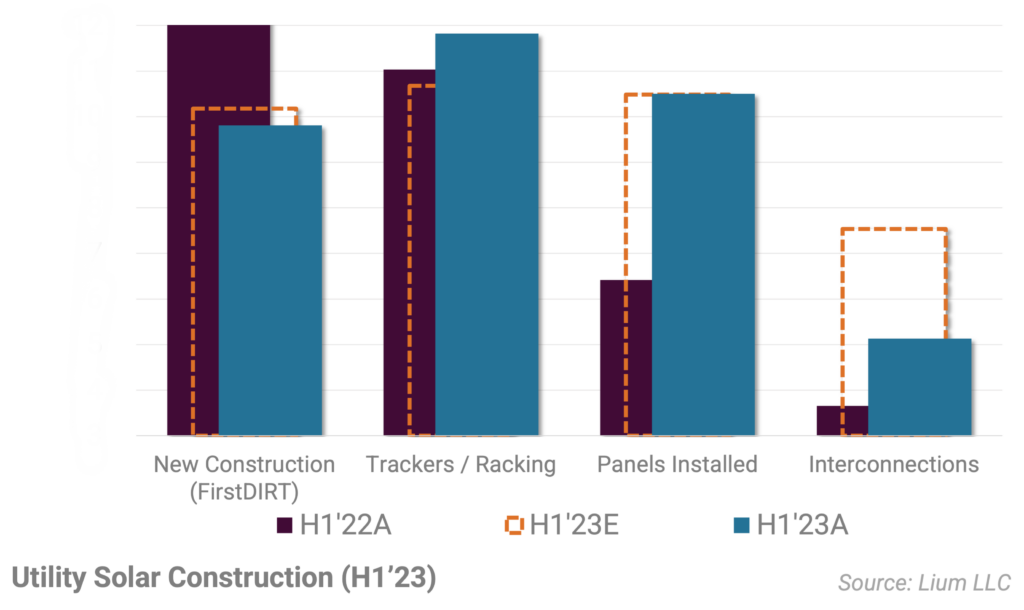

Generally speaking, solar generation has been disappointing in H1’23, increasing by a modest 7% (lagging the 20% growth in solar capacity over the same period).

Model update – H1 Firm, H2 Risks

Although we are still waiting on final June data, utility scale construction metrics have generally been mixed relative to our original expectations for H1’23.

SOLARSAT™: May construction picking up speed, but panel installations still falling behind

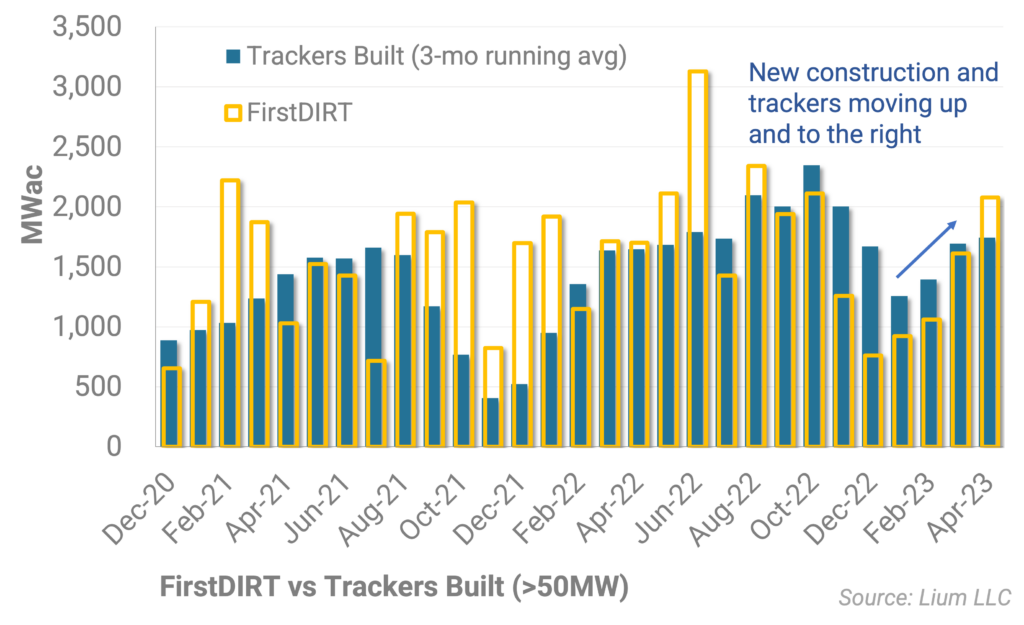

While new construction starts and tracker activity is progressing as expected in Q2, the conversion to panel installation is concerning.

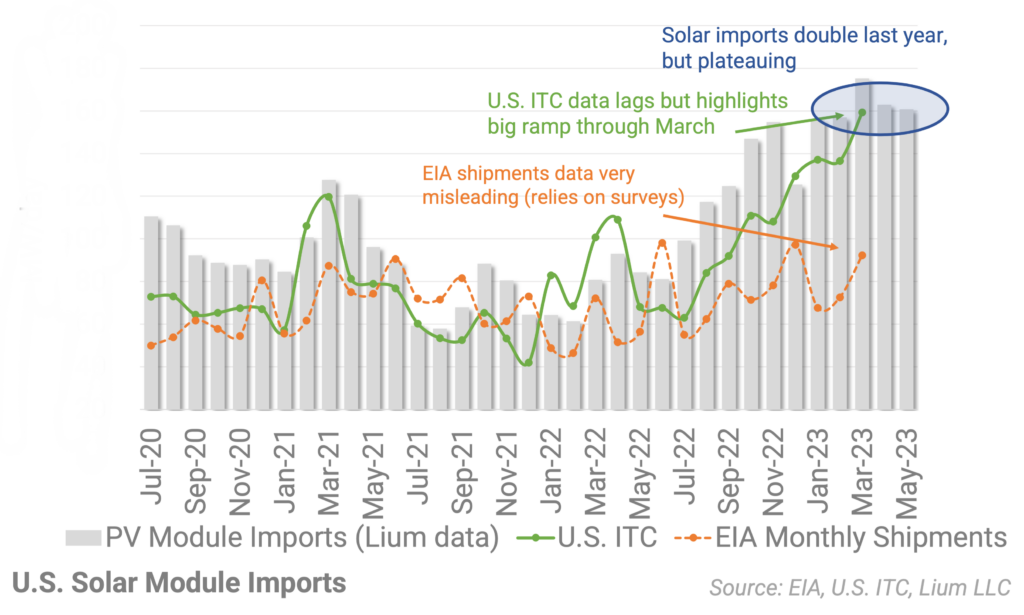

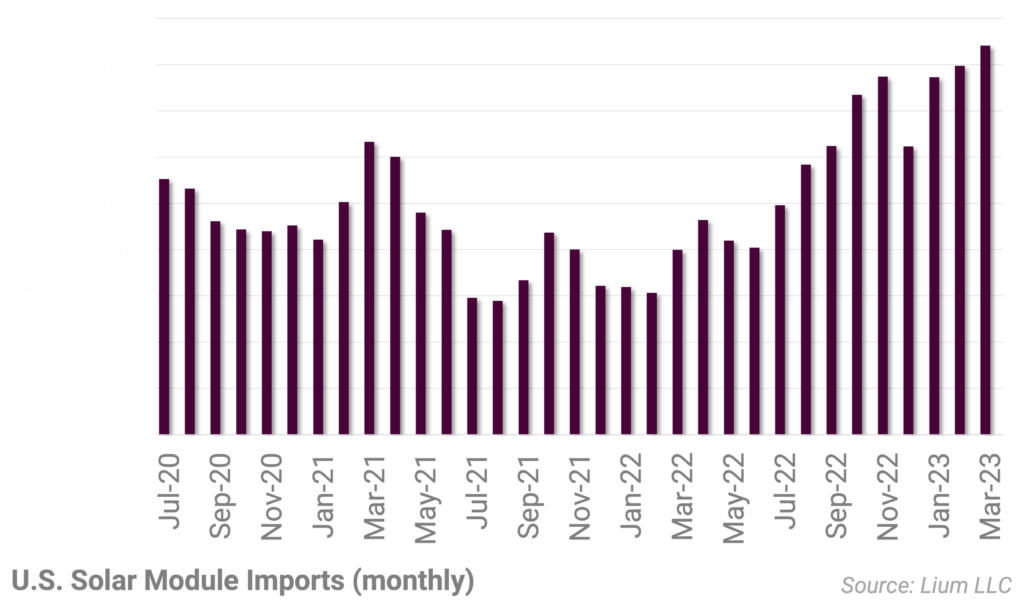

Import flows still good, but decelerating

The U.S. imported roughly double the volume of solar modules in April and early May compared to a year ago.

SOLARSAT™: Great April for new construction starts; Panel flows disappointing

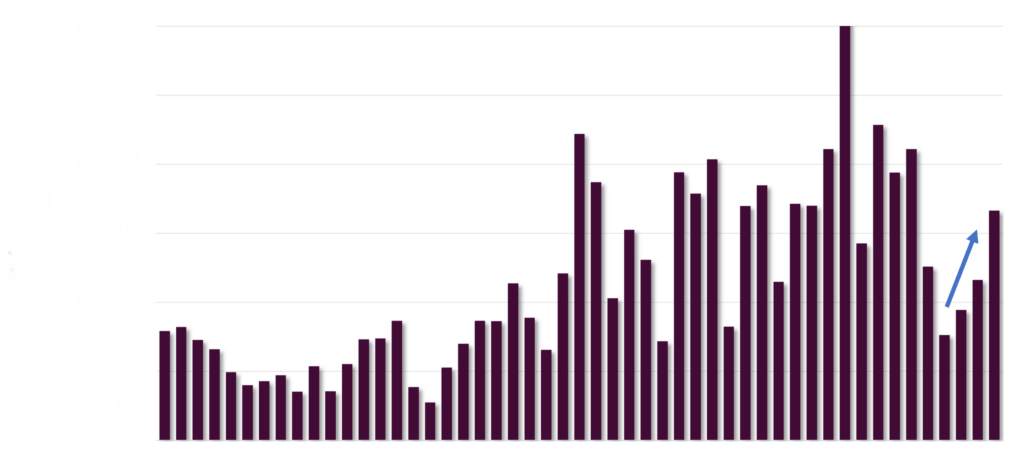

After a relatively slow winter, April new construction starts have picked back up to ~25 GWac annually.

SOLARSAT™: March new construction improves sharply (after slow winter)

In total, we identified around 1.6 GWac of new projects kicked off during the month

Takeaways from Austin RE+ Conference

After a strong Q1, leading edge anecdotes at the Austin RE+ conference suggest that new inbounds are coming to a halt in California.

March imports continue to be strong; Cambodia (BYD, New East) big growth; Avoid EIA Monthly Shipments Report (it is wrong)

India, South Korea, and Cambodia imports have been particularly notable, collectively up 400% compared to a year ago.