UTILITY SOLAR NOTE TO CLIENTS 072726

In this note, we are updating our utility-scale solar data and forecasts… latest trends in construction starts, approvals, crew counts, and market share… Broad takeaways from this update has been… to early stage indicators like applications and approvals while… construction activity and crew counts.

SOLARSAT™ NOTE TO CLIENTS 071026

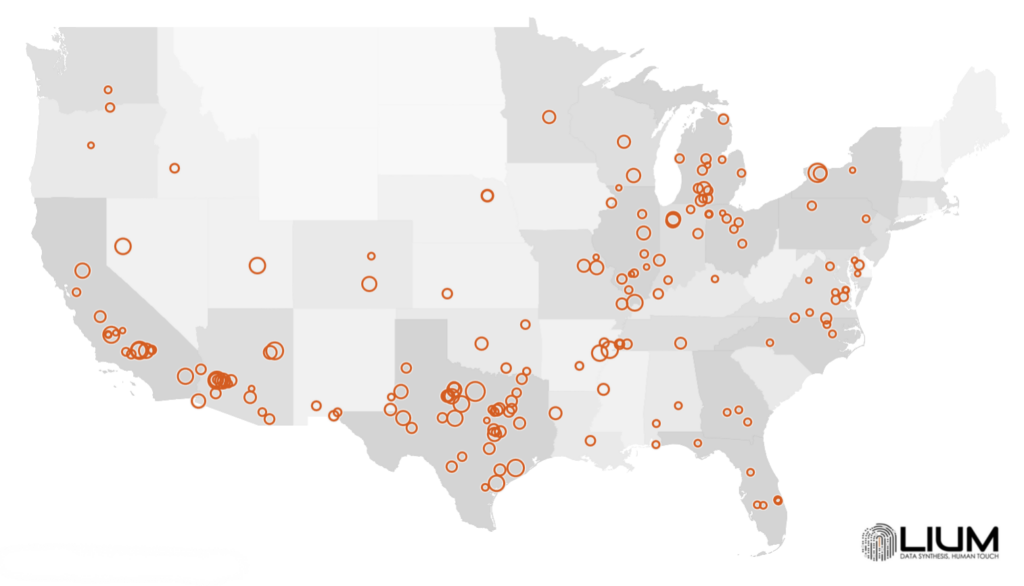

In this note, we refresh our monthly satellite and on-the-ground datasets, with June updated for FirstDirt, Trackers, Panel Installations, and Interconnections…

SOLARSAT™ NOTE TO CLIENTS 061026

In this note, we refresh our monthly satellite and on-the-ground datasets, with May updated for FirstDirt, Trackers, Panel Installations, and Interconnections…

UTILITY SOLAR NOTE TO CLIENTS 060126

In this note, we update our Q2 solar development data, paying closest attention to 1) new project applications 2) projects moving into pre-contract phase and 3) projects being approved to the late stage pipeline.

SOLARSAT™: April new starts light @ 2.8 GW (lots of projects, but all small); Midwest ramp begins; crews jump

In this note, we refresh our monthly satellite and on-the-ground datasets, with April updated for FirstDirt, Trackers, Panel Installations, and Interconnections…

Data refresh (Q1 / 2026); Construction on track; Module install ramp; New applications still main concern

In this note, we are updating our utility solar quarterly data and forecasts to reflect the latest trends in construction starts, approvals, crew counts, and market share… cycle remains firmly intact… construction starts running better than expected… approvals and orders stronger… domestic module demand (and supply) is ramping…

SOLARSAT™: Record March (4.5 GW New Site Work); Nextracker & SOLV share gains

In this note, we refresh our monthly satellite and on-the-ground datasets, with March updated for FirstDirt, Trackers, Panel Installations, and Interconnections…

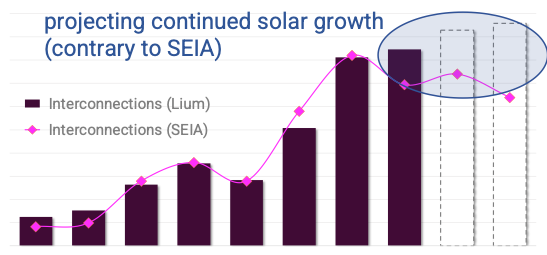

SOLARSAT™: EIA 860M (SEIA) is broken, ignore it; 2026 grows 10+% (albeit ho-hum start w/ low tracker installs); Nextera adds new Mortenson work

In this note, we refresh our monthly satellite and on-the-ground datasets, with February updated for FirstDirt, Trackers, Panel Installations, and Interconnections… We have also reviewed the SEIA / Woodmac report published this week…

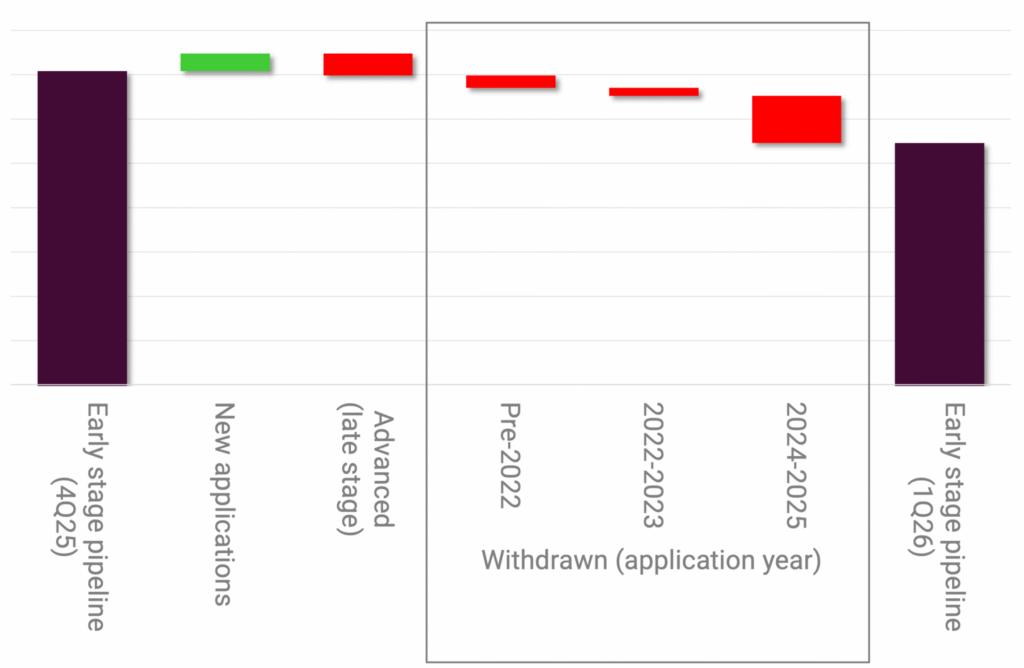

Approvals inflect higher (25 GW this qtr); Visibility through 2027E; But new applications have dried up

In this note, we summarize our takeaways after processing the last three months of applications, permits, and approvals… utility scale solar is pacing ahead of schedule in the near / medium term… increasingly concerned about growth thereafter.

SOLARSAT™: Slow construction start (lot of bad weather); Solar crews drop 12 to 208; Solv starts massive Swenson project; Gamechange taking share

In this note, we provide an update on construction activity since the beginning of the year… Despite the slow start, we are still anticipating 2026E to post strong utility-solar construction growth… with orders and backlog also ticking higher.