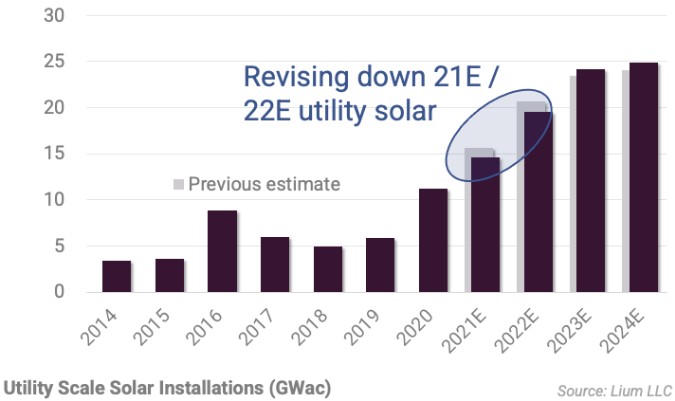

After taking in recent datapoints, we are updating our quarterly utility scale solar model (click here), noting a number of big projects that have been delayed in recent months. The recent delays have been driven by cost increases and supply chain challenges, key concerns NextEra highlighted this week in their letter to the U.S. Commerce Department seeking to unmask a pro-tariff group. Sourcing in some cases has also become more difficult as companies avoid potential risk out of the Xinjiang region.

Lowering Utility Solar 2021E / 2022E. With cost and supply chain challenges likely to remain elevated, we are lowering our 2021E and 2022E utility scale solar projections as jobs get backed up and potentially pushed to the next calendar year. Specifically, we are reducing 2021E and 2022E installations to 14.5 GW and 19.5 GW, respectively, down ~1 GW from our previous estimate. Other takeaways from our recent model update include…

***In Q2’21, 2GW of utility scale solar was installed in the U.S. This is up slightly from a year ago, but lower than our original estimate of 2.7 GW and below the peak of 5.3 GW in Q4’20.

***Some of the most notable delays have been in Texas, with several mega-projects being pushed 3-6 months.

***53 GW of utility scale solar is now online in the U.S., accounting for 3% of electricity usage in July.

***New construction starts have also been disappointing. With that said, the next few months are historically more active for kickstarting projects.

Utility Solar Still Has Best Upside. Although we are lowering our estimates, we are still well above consensus and think the market is underestimating 2022E and 2023E utility solar potential. In fact, based on what has entered the queue over the last 18 months, the U.S. could be soon be adding 25 GW per year of utility scale solar, almost double the current run rate. For more on our utility scale solar outlook, click here. FSLR, ARRY, FTSI, and SHLS are most leveraged to U.S. utility scale solar market.