2025 modest construction growth (+7%); Growth reaccelerating this year (CA, Northwest, Georgia); PRIM boost last year, MTZ on deck

Construction activity for large scale FTM battery storage increased modestly to… GW in 2025… We are projecting battery storage construction growth to reaccelerate into the… per year range in 2026/2027

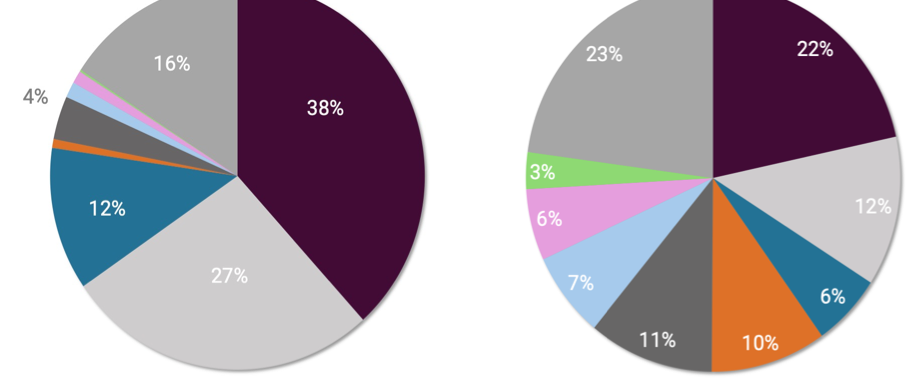

Data refresh & 2026E projections; EPC mkt share favors MTZ (PWR lower 2025); Gamechange takes back share

In this note, we are updating the latest utility-scale solar data, which includes our projections for industry metrics such new approvals / construction / installations and company specific such as EPC / tracker / module market share…

SOLARSAT™: 2025 wraps up as expected (35 GWac new site work); Installs take holiday break; Primoris spotlight (market share + efficiency gains)

In this note, we summarize the latest utility-scale solar satellite and field level data trends. Broadly speaking, the end of the year wrapped up about as expected with another…

SOLARSAT™: Panels on full tilt (9 GW installed last 3 months); Solar crew efficiency up 5-10% this year; FirstDIRT firm

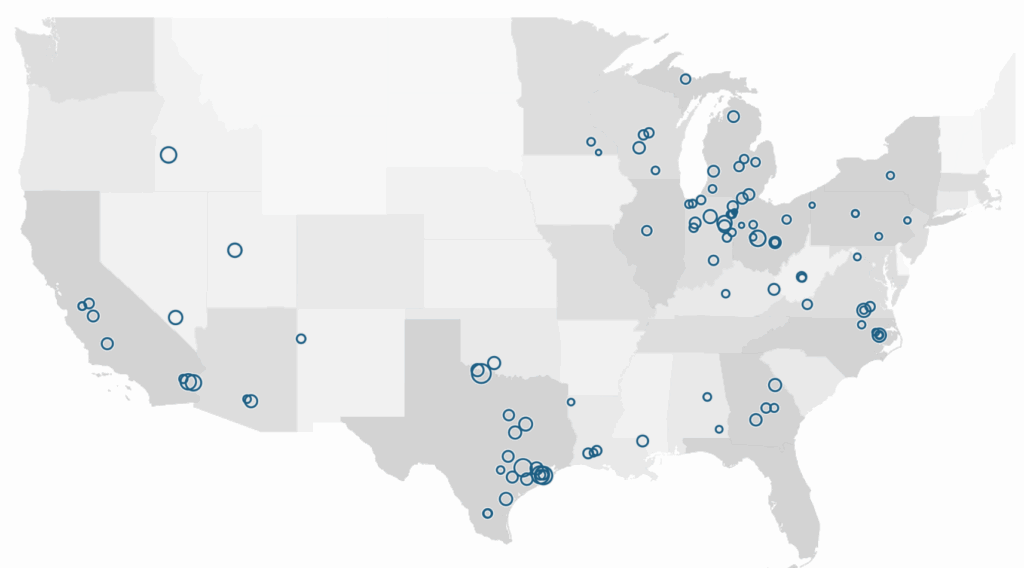

Solar crew count was flat again at ~230 in November compared to October. Compared to last year, the crew count is up 15%, driven by crew adds in Arizona, California, and Louisiana.

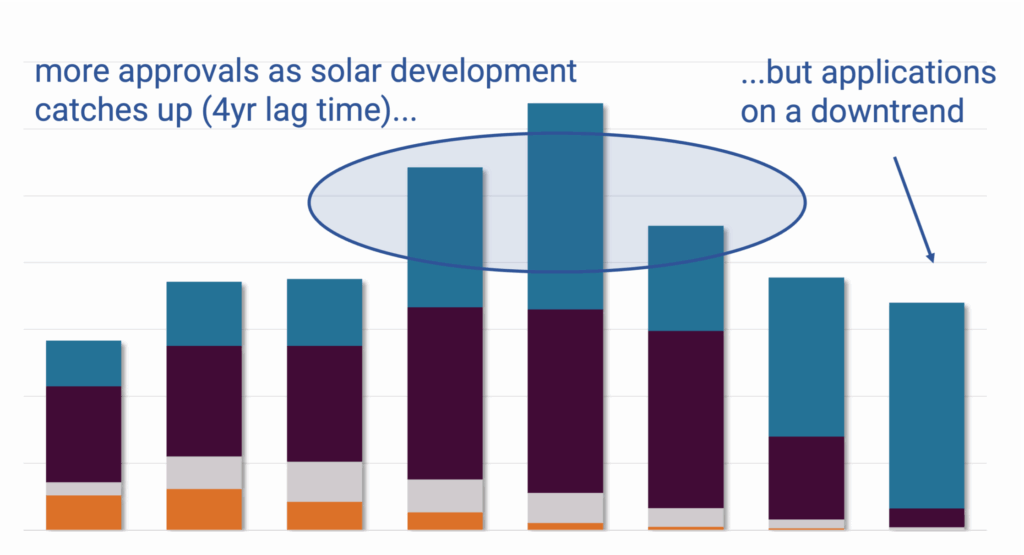

Solar train is rolling (RECORD 18 GW approved this quarter); Increasing 2027E construction projections; Applications on a downtrend

In this note, we summarize our utility-scale solar data after processing the last 3-months of construction, approval, and application filings….

SOLARSAT™: Construction momentum remains firm (October +25% y/y); Arizona big month

October utility scale solar projects started construction… very firm for this time of year, tracking up… Solar crew count was flat… EPC crews in California have been the standout…

BESS construction firm Q3; double digit growth through 2027; ERCOT red flags; Tesla big share gains

In this note, we are updating our BESS data for the latest construction and approval data.

Increasing 2026E projections (+10-15% y/y); Implies 50-60 more crews needed; Market share adds (Nextracker, Mastec, First Solar)

In this note, we are updating our utility-scale solar model (LS-1) which includes 2026E / 2027E projections for construction, solar crews, trackers and interconnections…

SOLARSAT™: Q3 wraps on high note (tracker installs +20% y/y); Crew efficiency-big gains driven by big EPCs; 2026E thoughts

In this note we 1) update our September construction activity 2) provide color on the latest EPC crew efficiency data and 3) take a glance at 2026E.

SOLARSAT™: Not yet seeing post-OBBB construction surge; Surprisingly SLOW TEXAS – driven by a MAJOR problem; PJM solar FINALLY taking flight

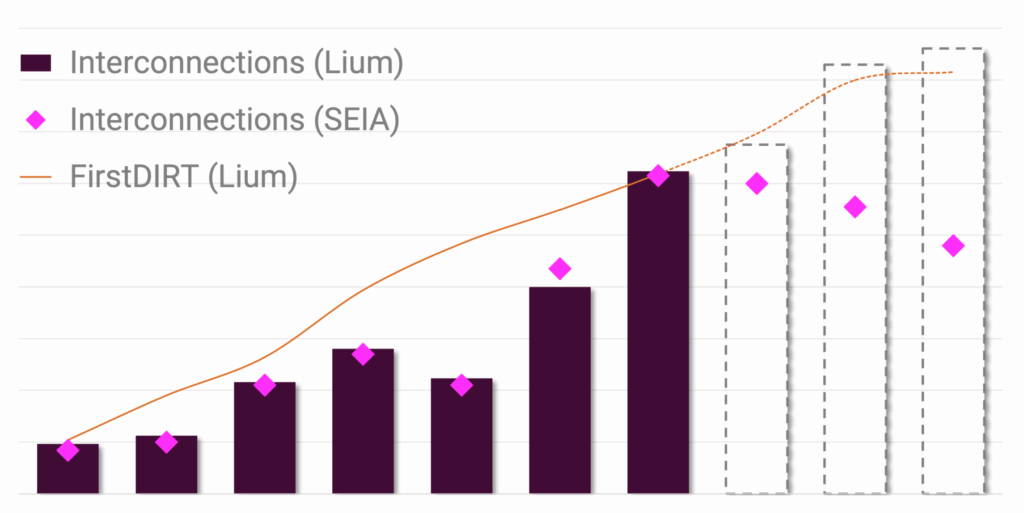

Contrary to the SEIA / Woodmac report this week… we are anticipating a big boost to solar installations (interconnections) through 2028E…