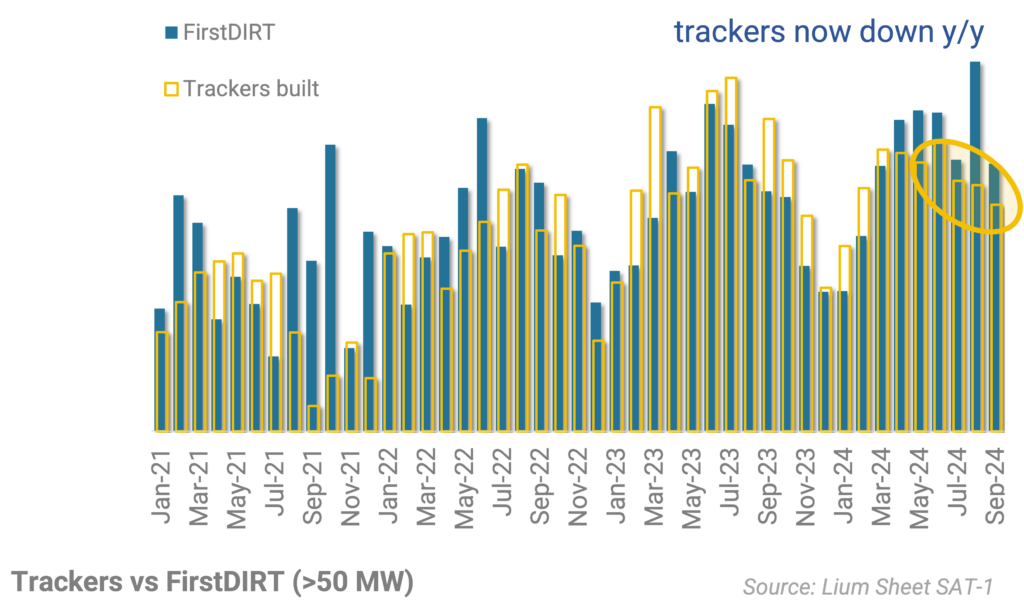

SOLARSAT™: Active December for site prep; PJM signs of life; Trackers land down 7% full year; Construction delays update

Below see key takeaways after going through our utility-scale solar satellite data for the month of December.

SOLARSAT™: Tracker activity very slow; Companies pulling 2025 installs forward; New construction chugging along

Below see key takeaways after going through our utility-scale solar satellite data for the month of November.

Interconnection approvals rebound…driven by big projects in desert states…benefitting from wave of queue requests 3-5 years ago

Following a slow start to 2024, interconnection approvals have rebounded since June.

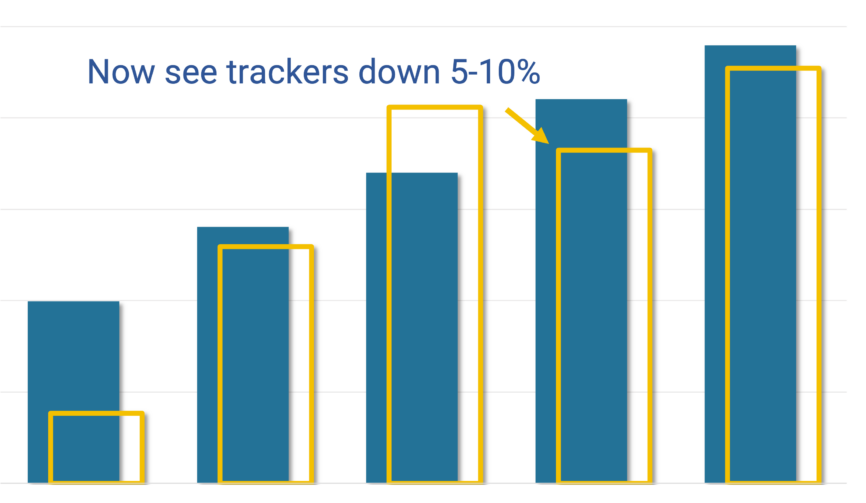

SOLARSAT™: Oct solar construction of soft side (<2GW); 85% new activity in Trump states; Trackers on pace for down 5-10% y/y

Little less than 2 GWac of new projects kicked off during October

Another 4GW new construction starts (on track for 30% growth this year); Texas almost half; FLNC, TSLA, CSI share gains

With three quarters in the books, the U.S. utility scale storage market is on track to land +30% this year, not too far off from original expectations and better than most other renewable sectors.

Modest summer rebound; October noticeably lower; 2025E projection @ +5%

With more than half of October now in, we are updating our Q4 and 2025E residential solar projections (RS-3).

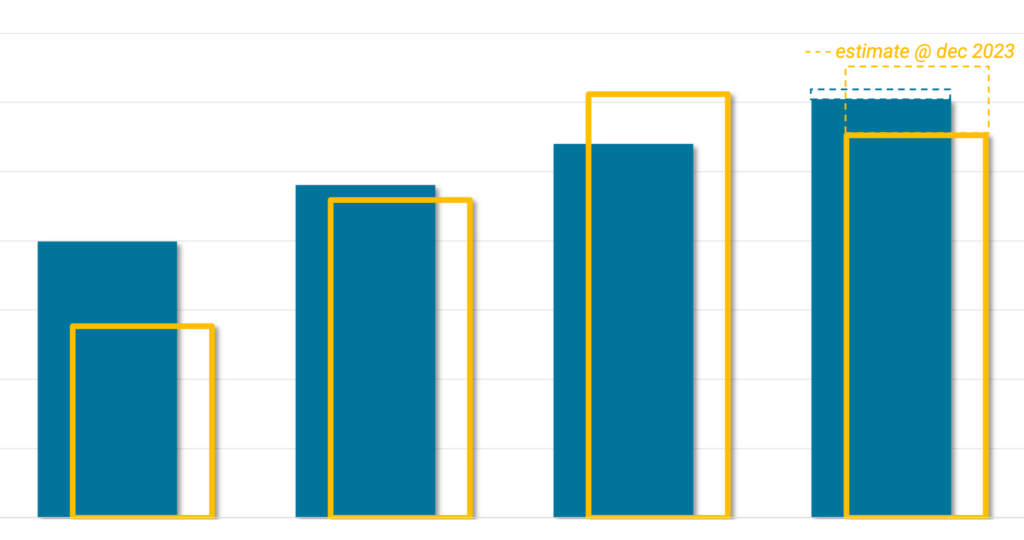

Model update…2024 trackers DOWN 5-10% (new construction +15%); 2025E signs of +10-20%

In this note, we are updating our 2024/2025 Utility Scale Solar Model (LS-1) after putting in actuals through September and refreshing our project / developer level forecast.

SOLARSAT™: September new starts firm again (2.6 GWac); Q3 lands +12% y/y; Tracker installs soft

After a record August, September new construction has remained firm. Specifically, 2.6 GWac of new projects kicked off construction during September, down from almost 4 GWac last month, but still tracking well ahead of last year.

Refreshing data sheets to reflect latest construction starts (LS-2, PLUS-201); 2025E tracker outlook improving

In this note, we are updating our LS-2 and PLUS-201 files to reflect the latest satellite and company data.

SOLARSAT™: Huge August for new construction starts (3Q tracking +20% y/y)

After a disappointing July, new construction starts have seen a huge bounce in August. In fact, almost 4 GWac of projects kicked off during August, the best month of activity for U.S. utility solar so far. For 2024E full year, new construction starts are very much on track to hit our original projection of 15-20% y/y. Meanwhile, tracker demand has not yet caught up to new construction starts and remains on track for flat 2024E.